Account-to-account payments for ecommerce – pros and cons

by Gosia Furmanik on December 29, 2021

Open Banking for online payments

With the rapid growth of online shopping, ecommerce companies face ever increasing competition and therefore must look into all opportunities to preserve and improve their margins. Payment processing fees often run at 2-3% of the transaction value, eating into the margin. With account-to-account payments, ecommerce businesses can cut payment processing costs by up to 85%.

Account-to-account payments are, effectively, instant bank transfers. Since PSD2 was implemented in the EU and UK, account-to-account payments have become a viable alternative to card payments. Regulated third party providers, like fena, offer payment products including payment API aggregators and payment gateways which utilise the banking ecosystem.

What's PSD2?

PSD2 stands for Payment Services Directive Two. It’s a revised payment legislation introduced in 2018 in the EU and the UK. This updated law has added extra requirements like Strong Authentication and mandated that banks open their information and payments APIs to third parties.

But what are the pros and cons of Open Banking payments for ecommerce businesses?

Pros:

Reduced costs of transaction

– as Open Banking allows third party providers to utilise existing banking infrastructure to provide payment solutions, bypassing card schemes, expensive card processing fees are removed.Instant settlement

– in the UK and many other European countries, bank transfers are instant; Open Banking payments take advantage of this.More secure

than card payments – no card details or bank details are stored by the third party provider or merchants, reducing the risk of fraud.

Cons:

Non-reversible transactions

as it relies on bank transfers. This can impact ability to process refunds.No chargeback mechanism

– this is a double edged sword as merchants like the lack of chargeback mechanism; however with such a setup there are no extra protective measures for consumers in case of payment disputes.Requirement of Strong Authentication for each transaction

– no transaction is authorised without at least two types of authentication: registered device and face ID, fingerprint or a pin.

How it works in practice

An ecommerce website can add open banking payments as an option at the checkout. By integrating the fena open banking payments API or gateway, merchants can quickly and easily start taking account-to-account payments.

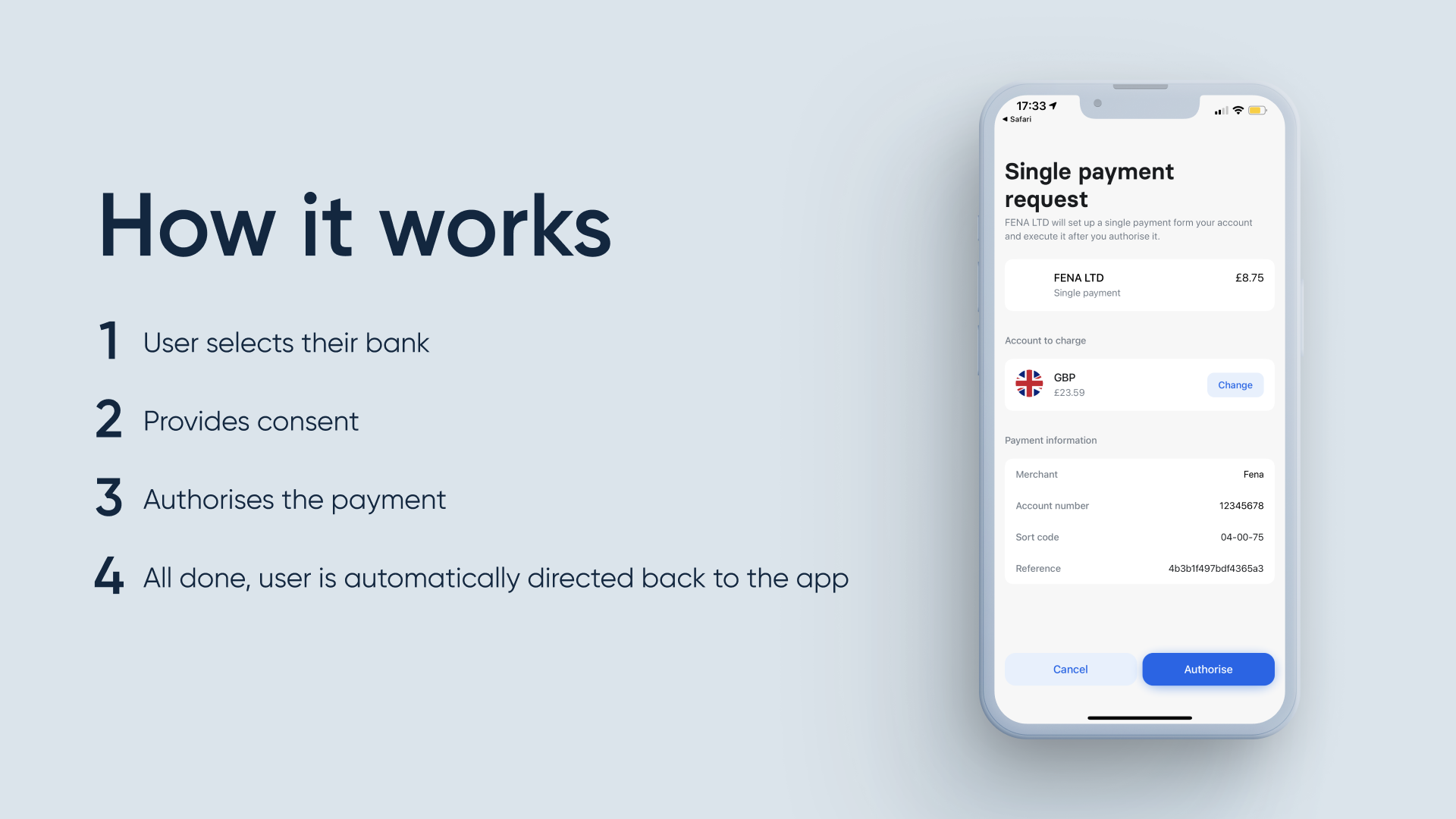

How does it work for a consumer?

Step 1

– A consumer chooses to pay with ‘Instant Bank Transfer’Step 2

– The consumer is taken to a page where they select the bank they want to pay with.Step 3

– Then, they are redirected to their online banking on desktop or banking app on mobile.Step 4

– On mobile, they can confirm the transaction with their Face ID/Fingerprint/PIN. On desktop, they can log in into their online banking or scan a QR code to complete the transaction on mobile.Step 5

– If the transaction is successful, they will be redirected to the confirmation page.